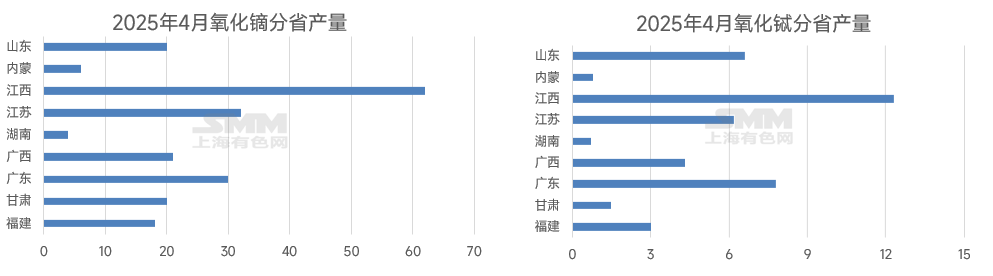

SMM News on April 18: On April 4, 2025, the Ministry of Commerce and the General Administration of Customs jointly issued an announcement to implement export controls on seven categories of medium-heavy rare earth-related items, including samarium, gadolinium, terbium, and dysprosium, covering various forms such as metals, alloys, and permanent magnet materials.

As the dominant force in the global rare earth supply chain, China controls approximately 85% of the global smelting capacity. This control directly led to an expansion of the supply gap for medium-heavy rare earths in overseas markets, particularly affecting key varieties such as dysprosium and terbium. Developed countries like the US, Europe, Japan, and South Korea have a high degree of dependence on China's supply of medium-heavy rare earths. For example, 70% of the rare earths imported by the US come from China. As of now, within one month after the implementation of rare earth export controls, overseas prices for medium-heavy rare earths have surged rapidly. In the past month, the price of dysprosium oxide in Europe has nearly tripled, while the price of terbium oxide has more than doubled. However, domestic prices for dysprosium and terbium have remained stable, further widening the price spread between domestic and overseas markets.

According to the SMM survey, some industry participants have high expectations for domestic dysprosium and terbium prices, believing that the sustained rise in overseas prices in the short term may spill over to the domestic market. Moreover, the current supply of rare earth ores from Myanmar remains very limited, and with the arrival of the rainy season in Southeast Asia, the domestic supply of medium-heavy rare earths may also decline. From the perspective of upstream producers, the domestic medium-heavy rare earth market may face a situation of weak supply and demand in the short term. Enterprises need to pay attention to the issuance of smelting and separation indicators as well as their own production rhythms. From the demand side, restrictions on the export of high-performance NdFeB permanent magnets may affect the international high-end manufacturing supply chain. However, it is worth noting that domestic policy-driven development of end-use industries may continue to drive the growth in demand for NdFeB, which will support the supply-demand balance of rare earth products.

Considering all aspects, China still holds a dominant position in rare earths through its capacity and technological advantages. The reconfiguration of overseas supply chains may spur breakthroughs in alternative or recycling technologies, but it will be difficult to change China's dominant position in the short term. The supply shortage and price increases for dysprosium and terbium have become inevitable in the short term.

》Apply for a Free Trial of SMM Metal Industry Chain Database